Copper retreated on the London Metal Exchange after weeks of gains, reflecting rising geopolitical tension as fragile ceasefire negotiations between Washington and Tehran approach a critical deadline, a development that YourDailyAnalysis identifies as a turning point for commodity sentiment. The benchmark metal slipped 0.5% to $13,275 a metric ton, while broader industrial metals followed lower as oil reversed prior losses, underscoring renewed macroeconomic anxiety.

The immediate trigger lies in uncertainty surrounding the Strait of Hormuz, a vital corridor for global energy flows. With maritime transit sharply reduced amid escalating conflict, fears of prolonged disruption have intensified. The strait handles roughly a fifth of global oil shipments, and any sustained blockage risks amplifying already volatile energy prices. For industrial metals, the transmission mechanism is indirect but powerful – higher energy costs raise production expenses and constrain manufacturing output, weakening demand fundamentals.

China’s demand profile has offered partial insulation against these pressures. Inventory levels on the Shanghai Futures Exchange have fallen by nearly 200,000 tons since mid-March, reflecting strong seasonal consumption and tight domestic supply. This divergence between Western macro concerns and Asian demand resilience has created a fragmented pricing environment, where localized strength competes with global risk aversion. YourDailyAnalysis continues to track this imbalance as a defining feature of the current metals cycle, particularly as Chinese consumption remains the dominant marginal driver.

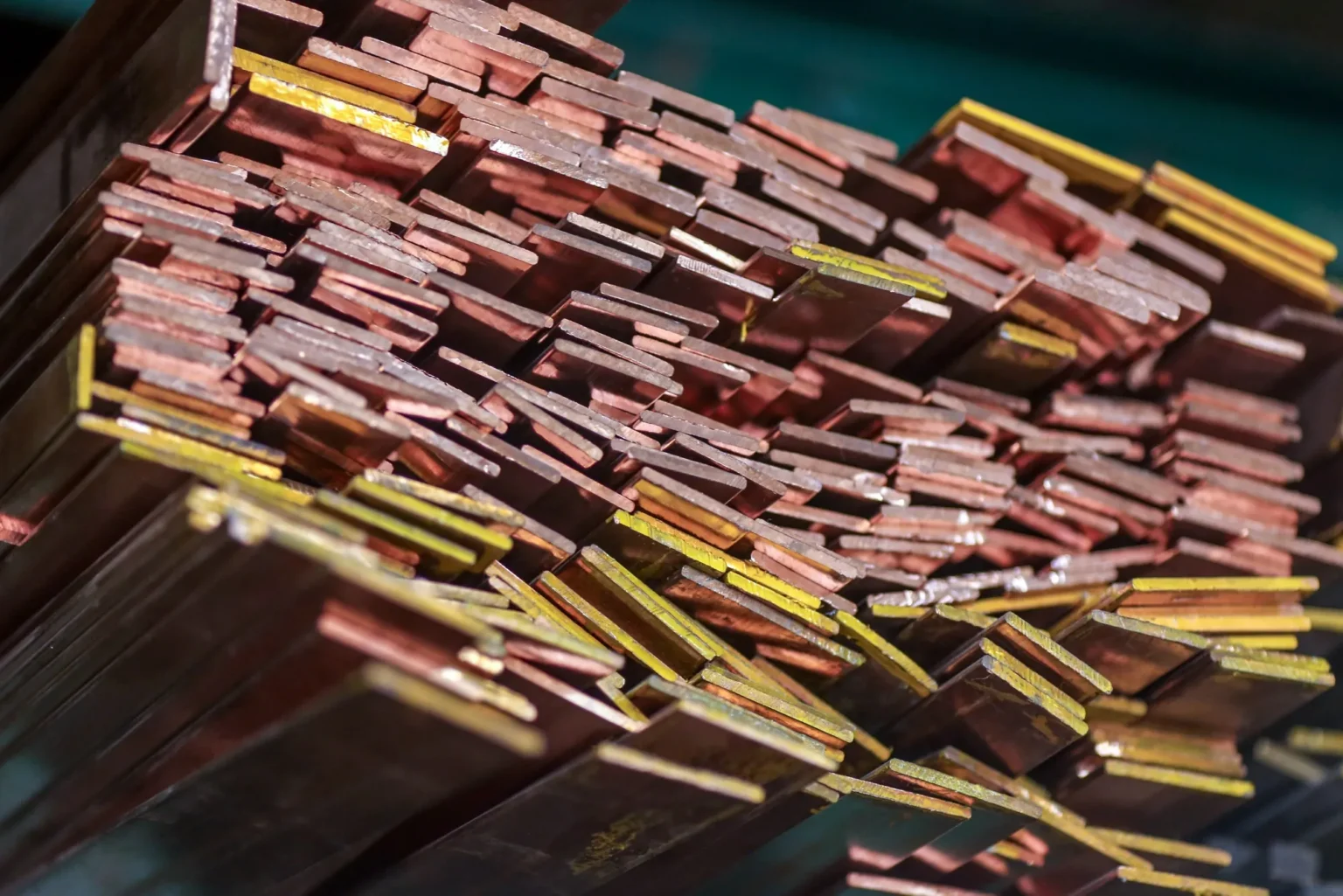

Aluminum markets reveal a contrasting dynamic shaped more directly by supply disruptions. Production cuts across Gulf smelters, triggered by logistical constraints and restricted access to raw materials, have tightened availability. The U.S. Midwest premium surged to a record $1.14 per pound, signaling acute regional shortages despite broader uncertainty. YourDailyAnalysis highlights how this premium reflects structural bottlenecks rather than speculative pressure, indicating that supply chain fragmentation now plays a central role in price formation.

The geopolitical dimension complicates monetary policy expectations. A sustained energy shock could push central banks toward a more restrictive stance, prioritizing inflation control over growth support. Such a shift would exert additional pressure on industrial demand, particularly in sectors sensitive to financing costs such as construction and infrastructure. The interaction between energy volatility and monetary tightening introduces a second-order effect that extends beyond immediate commodity pricing.

Meanwhile, aluminum’s relative strength – still up 13% since the conflict began – demonstrates how supply-side constraints can override demand concerns in specific markets. The inability to restock raw materials or export finished goods from affected regions has created cascading disruptions, stretching supply chains as far as Australia. These frictions reinforce the notion that geopolitical risk now operates not only through pricing channels but also through physical trade flows.

As negotiations over the ceasefire remain unresolved and shipping routes stay constrained, commodity markets face a dual uncertainty – one tied to demand erosion through macroeconomic channels, and another rooted in supply dislocation. Your Daily Analysis frames this moment as a recalibration phase where pricing increasingly reflects logistical realities rather than purely financial expectations, leaving metals exposed to sudden shifts driven by political developments rather than traditional market signals.