By mid-2026, more than eighty large-scale AI projects will be under construction simultaneously – the highest level of concurrent infrastructure activity in recorded history. The implications ripple far beyond the technology sector. YourDailyAnalysis frames this as the second-order story markets have not yet fully priced: the AI buildout is reshaping construction economics, labor markets, and real estate in ways that affect companies well outside the Nasdaq.

Start with the physical constraints. Data center construction requires high-voltage electrical transformers that currently run on 12-to-24 month delivery timelines. That single component is the most cited cause of project delays. The constraint ripples through adjacent builds: a hospital planning a bond-funded capital project may discover that nearby data center developments have absorbed the regional labor pool, inflating wage costs for electricians and HVAC technicians by 30% to 60%. A school district in the same power corridor as a new AI campus faces infrastructure competition it never modeled.

The labor dimension is acute. Industry estimates put the global additional requirement at more than 200,000 electricians, technicians, and project managers by 2026. Liquid-cooling systems and high-density cabling require precision closer to aerospace manufacturing than traditional construction. CBRE generated more than $3 billion in infrastructure-related revenue in 2025 and nearly $950 million in Q1 2026 alone. The reporters at YourDailyAnalysis trace the wage inflation in skilled construction trades directly to the AI capex cycle.

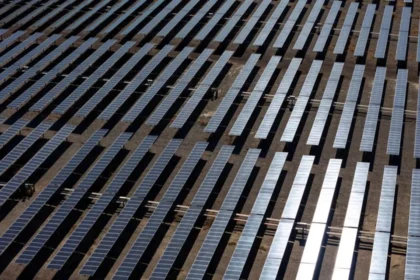

Power is the binding constraint that makes the transformer shortage feel manageable by comparison. Grid capacity is local, regulated, and can take three to five years to expand. Sean James, distinguished engineer for energy systems at Nvidia, described at Data Center World 2026 how training cluster load patterns ripple all the way back to the power plant, requiring generation to ramp in real time to match workload behavior. Operators are adding behind-the-meter generation as a stopgap while waiting for grid connections.

Real estate economics have shifted. Data centers are on track to surpass office construction as the largest category of new commercial building in the United States. Returns for data centers reached 11.2% in 2025, second only to manufactured housing. Quanta Services holds a record $44 billion backlog and covers the full electrical path from power plant to server rack. The team at YourDailyAnalysis identifies this convergence of construction, real estate, and energy as the most underappreciated economic consequence of the AI buildout.

Community opposition is intensifying across Louisiana, Arizona, Michigan, and Texas over water consumption, noise, land use, and strain on local power infrastructure. Bob Sulentic of CBRE acknowledged that opposition has intensified as the buildout accelerates, while arguing that projects will gravitate toward locations with the best power, water, and infrastructure fundamentals. That logic concentrates development in fewer locations, further inflating land costs and labor premiums in those markets, and creating a bifurcation between AI-ready regions and the rest.

Supply chain fragmentation adds a geopolitical layer. Specialized components face sourcing constraints that compound the construction timeline problem. Vertiv, which supplies liquid cooling and power distribution inside data centers, has consistently beaten guidance through 2026 with backlog visibility into 2027. The analysts at Your Daily Analysis spot this as the picks-and-shovels play most retail investors are still underweighting: companies that get paid regardless of which AI model wins.

Saudi Arabia’s Public Investment Fund has committed to AI campus developments that would move the buildout geography meaningfully outside the United States for the first time at scale. Countries with favorable energy profiles, existing industrial infrastructure, and government incentive structures hold a real structural advantage in attracting the next wave of construction and the economic activity that accompanies it.

What comes next is a supply chain stress test applied to physical infrastructure rather than software or semiconductors. The bottlenecks are measured in years, not quarters. YourDailyAnalysis leaves the operational question open: whether the buildout timeline catches the demand curve, or arrives late to a market that has already restructured its expectations around scarcity.